Turn $300,000 in Your Super Into a $1,000,000 Investment Property

Australians are quietly using their SMSF to buy investment property, build long-term wealth, and pay less tax — while their super does the heavy lifting. Find out in 5 minutes whether your fund qualifies and exactly how much you could borrow.

This is for you if you've got $150K+ in super, you're tired of average returns, and you want a clear answer on whether your fund could buy an investment property — without the broker jargon.

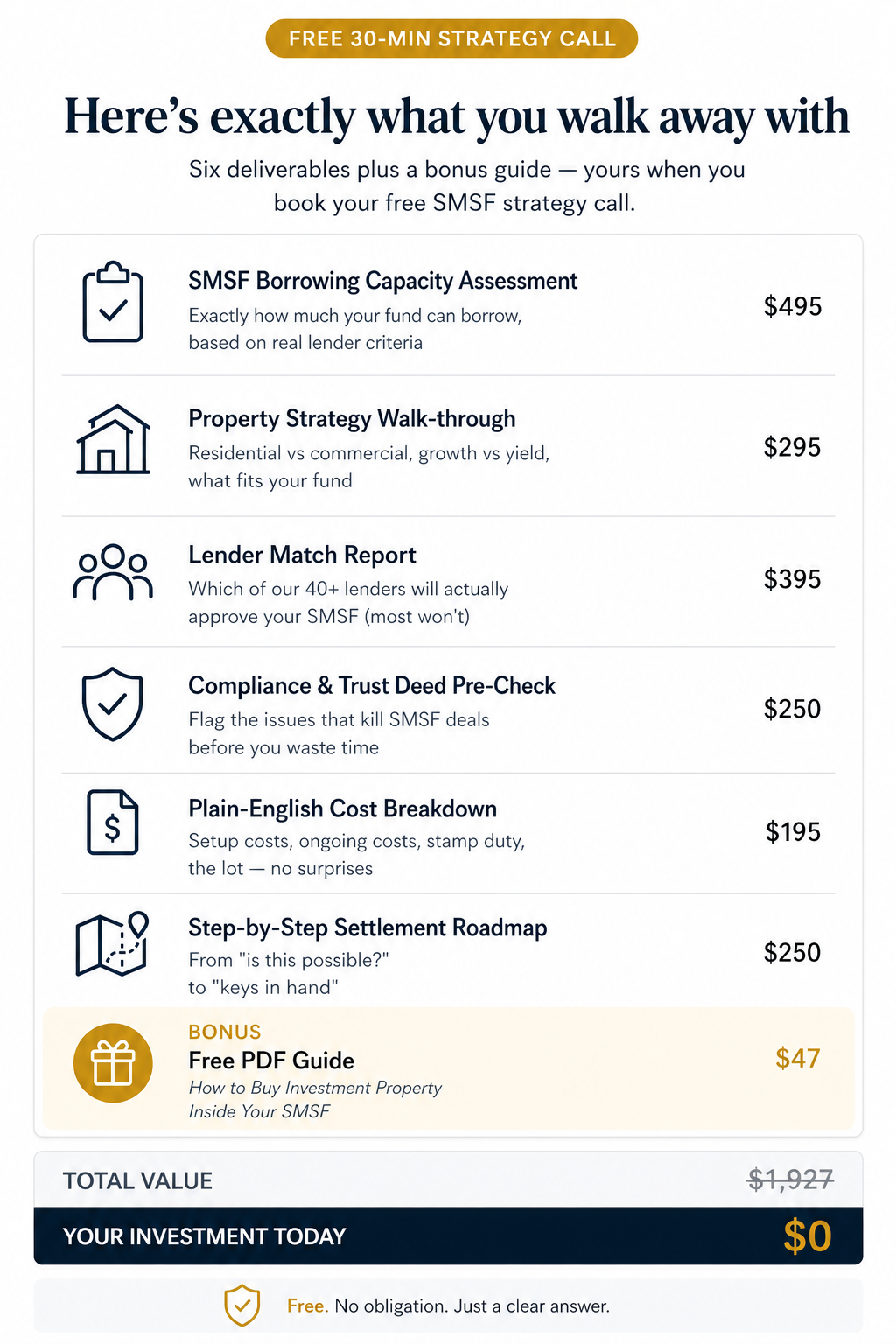

How it works

Book a call. Free 5-min SMSF strategy session. No obligation.

We assess your SMSF Eligibility, fund balance, trust deed & compliance check.

We source the right lender. Compare 40+ lenders. We find your best rate and structure.

Settlement. Investment property owned inside your SMSF. Done.

Not ready to book a call yet?

Download our free plain-English guide — How to Buy Investment Property Inside Your SMSF. Covers eligibility, costs, lenders, and the step-by-step process.

The maths most Australians have never been shown

Most people have no idea their super can be leveraged. Here's a typical scenario we see at Xskape Finance.

Sarah and Tom, both 42. Combined SMSF balance: $300,000.

They use $250,000 from their super as a deposit plus costs. Their SMSF borrows $800,000 from a specialist lender. They purchase a $1,000,000 investment property in Western Sydney.

Rent goes into the super fund. Loan repayments come out of the super fund. The property grows in value inside the fund's tax-advantaged environment.

What changed? Their $300,000 of super is now controlling a $1,000,000 asset — one they couldn't have bought personally without remortgaging the family home.

Illustrative example only. Outcomes depend on your fund balance, trust deed, lender criteria, and personal circumstances. This is general information, not personal financial or credit advice. Speak to us and your accountant before acting.