Lo Doc Home Loans · Self-Employed Specialists

Banks Said No.

We Know Another Way.

Being self-employed shouldn't cost you your property goals. Xskape Finance accesses 40+ lenders — including specialist Lo Doc lenders the big banks won't tell you about. Get a straight answer in 24 hours.

Sound familiar?

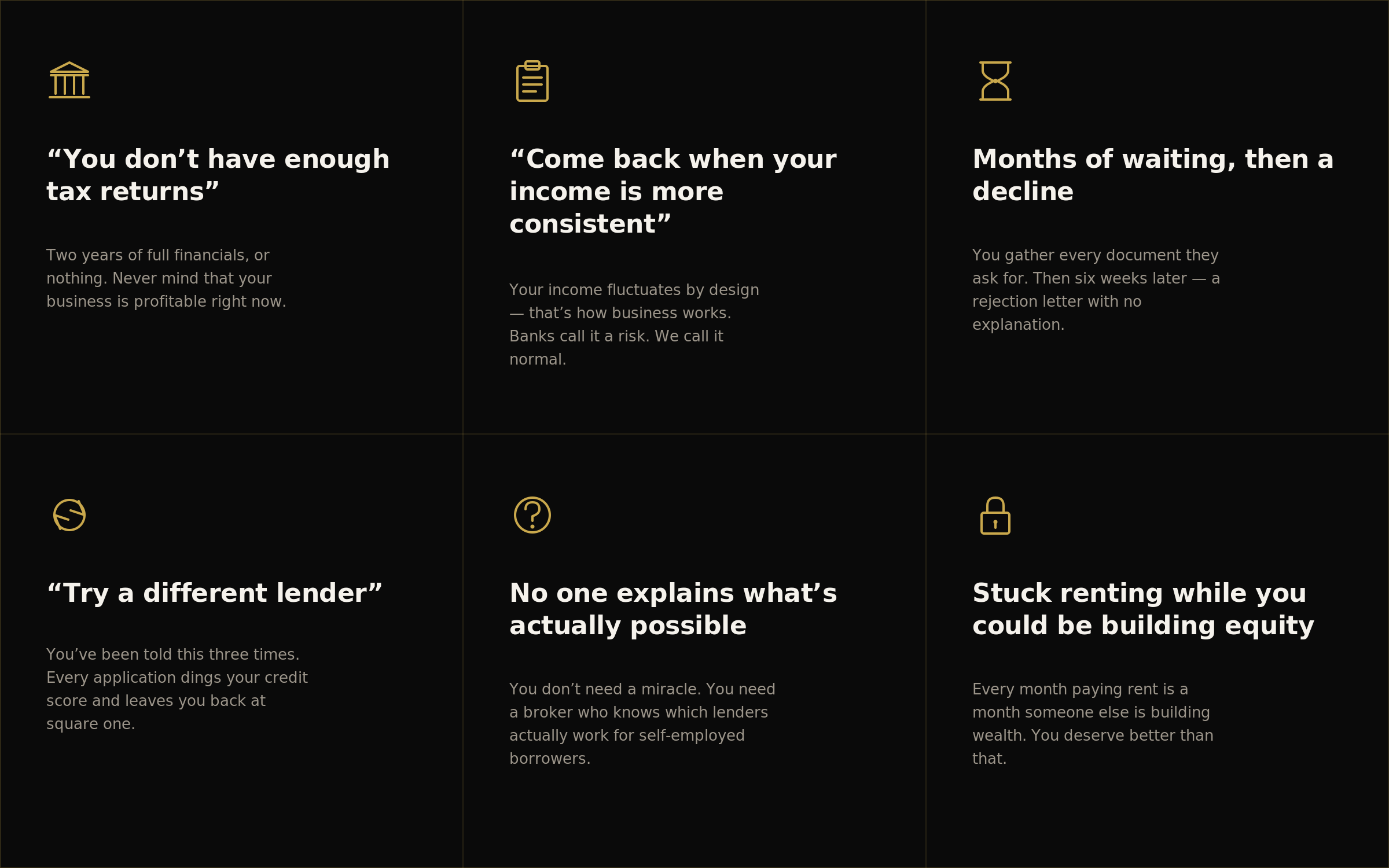

The Self-Employed

Loan Trap Is Real.

If you run your own business, the standard mortgage process was not designed for you. The banks score you on a model built for PAYG employees — then penalise you for not fitting the box.

Everything You've Been Wondering About Lo Doc Loans.

Straight answers — no jargon, no runaround.

-

No — that's the whole point of a Lo Doc loan. Unlike standard home loans, Lo Doc loans allow you to verify your income using alternative documents such as Business Activity Statements (BAS), business bank statements, or an accountant's letter.

Some specialist lenders on our panel accept as little as 12 months of BAS statements, depending on your situation. The exact requirements vary by lender — which is why working with a specialist broker makes a significant difference to your outcome.

-

Yes, in many cases. The major banks use rigid credit models built for PAYG employees — not business owners. Being declined is not a verdict on your creditworthiness. It means that lender's model doesn't suit your income structure.

Specialist lenders like Pepper Money, Liberty Financial, La Trobe, and Bluestone assess self-employed borrowers very differently. Book a free assessment before applying anywhere else — every credit enquiry affects your credit file.

-

Most clients receive a clear picture of their borrowing capacity within 24 hours of their free 30-minute assessment. You don't need documents ready for the initial conversation — we'll tell you exactly what to prepare afterwards.

-

Generally yes, Lo Doc loans typically carry a slightly higher rate — however the rate premium has narrowed significantly as specialist lending has become more competitive. Many clients refinance to a lower rate once full financials are available.

The exact rate depends on your LVR, lender, loan size, and financial profile. We provide a realistic rate range during your free assessment — no surprises.

-

At least one of: 12 months BAS statements, 12 months business bank statements, or an accountant's letter confirming income and self-employment status.

Standard across most lenders: ABN registered for 12–24 months, GST registration (if turnover exceeds $75,000), signed income declaration, and standard ID. The exact combination depends on which lender we match you with.

-

Yes — completely. Mortgage brokers in Australia are paid by lenders when a loan settles, not by borrowers. There is no cost to you at any stage of the process, regardless of whether you proceed. If we can't find a suitable solution, we'll tell you honestly and explain exactly what would need to change.